AMZN

🛒 Amazon’s e-commerce dominance, fueled by its vast logistics network and third-party marketplace, benefits from strong scale and network effects, with continued growth projected around 8% annually.

☁️ Amazon Web Services (AWS) is the primary profit driver, leading the cloud market with significant competitive advantages (switching costs, innovation) and robust future growth prospects, despite generating only 17% of total revenue.

💡 High R&D spending ($88 billion annually) may understate Amazon’s true profitability, suggesting potential undervaluation. The stock offers a similar estimated annual return potential (around 14%) as Alphabet but is perceived as having lower current risks.

@Invierteygana:

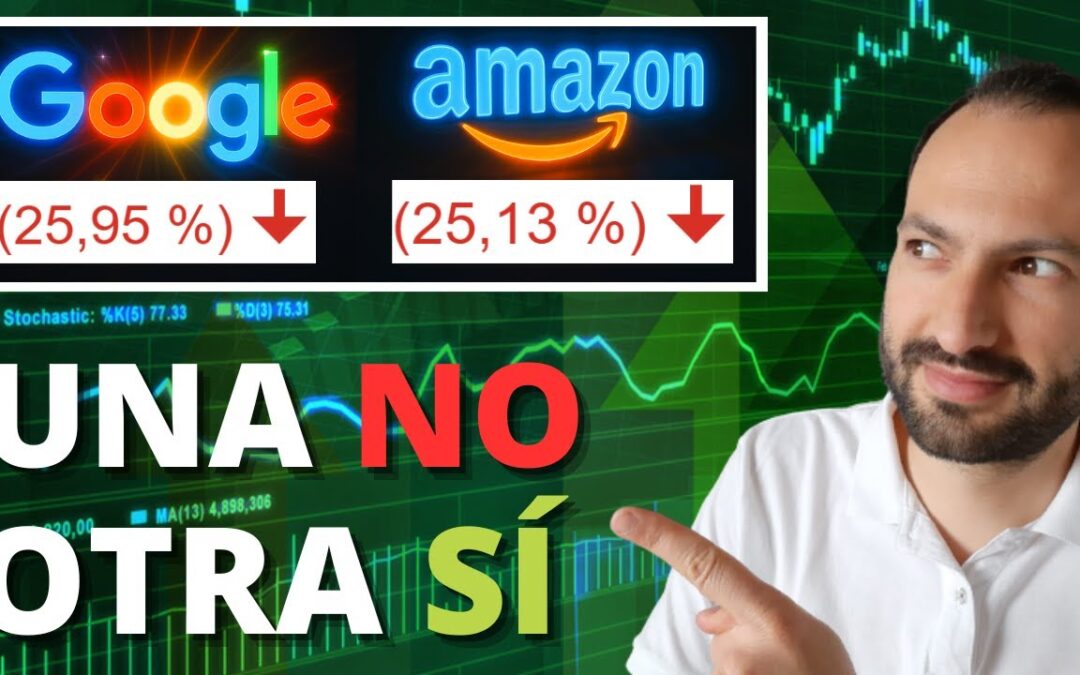

“Amazon, one of the world’s most valuable companies, has also fallen 25% from its highs. Its sales breakdown shows 39% from online product sales and 3% from physical stores (like Whole Foods). Another 25% comes from third-party sellers using Amazon’s platform, where Amazon earns commissions and offers logistics services (Fulfillment by Amazon). Amazon Web Services (AWS) accounts for 17% of revenue but generates the majority of profits. Subscription services (Prime, Prime Video, Music, Twitch) contribute 7%, and advertising makes up most of the remaining 9%. Amazon possesses strong competitive advantages: scale in its logistics network for online retail, which is hard to replicate, and the network effect in its third-party marketplace (more buyers attract more sellers, and vice versa). E-commerce continues to grow, potentially boosting Amazon’s sales by 8% annually. AWS benefits from high switching costs and market leadership, with Garner recognizing its innovation. This sector still has significant growth potential. Advertising is also growing across e-commerce and media platforms (Prime Video, Twitch). Overall, Amazon’s business is very solid with strong competitive advantages and growth capacity. Historically, revenues and profits have grown consistently, though 2022 saw a dip due to increased transport costs. Margins and ROE (Return on Equity) are improving, and the company has net cash. A key factor in valuation is its massive R&D spending ($88 billion), nearly double Alphabet’s or Meta’s. While some R&D is maintenance, a significant portion is likely investment in growth, meaning declared profits might understate true earning power, making the stock seem more expensive than it is. Considering this and its growth potential, the estimated 2029 profit could be $146 billion. Using a P/E of 25, the 5-year target price is $34, implying a 96% potential return, or over 14% annually. This is similar to Alphabet’s potential return, but Amazon is currently considered to have significantly less risk.”

Watch the exact part of the video where @Invierteygana talks about Amazon here:

Watch the video on YouTube

Read more articles analyzing Amazon (AMZN) at the provided link. AMZN stock.